1. What is Insurance?

Insurance is a Financial Product sold by insurance companies to safeguard you and your property against the risk of losses, damage, or theft (such as flooding, burglary, or an accident).

Insurance is the process by which the risk is spread, usually among a large group of people. Insurance is a form of risk management primarily used to hedge against the risk of contingent, uncertain losses.

The Pooling of fortuitous losses by transfer of such risk to insurers, who agree to indemnify the insured for such losses, provide other monetary benefits on their occurrence, or render services connected with risk. It is a system under which individuals, businesses, and other organisations or entities, in exchange for payment of the sum of money (a premium), are guaranteed compensation for losses resulting from specific perils under specified conditions.

2. Types of Insurance:-

There are two types of Insurance:

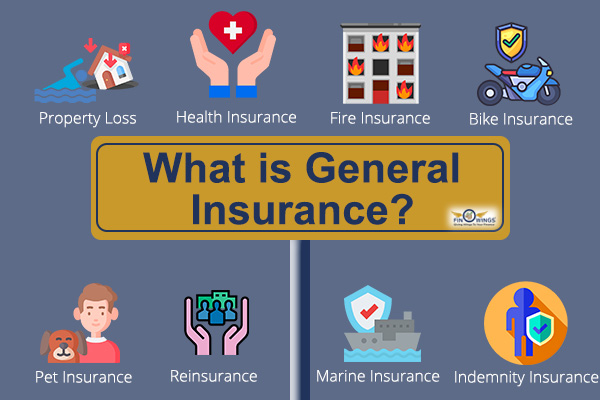

2.1 General Insurance:

2.1.1 Fire Insurance

A Fire Insurance is a contract under which the insurer, in return for a consideration (premium), agrees to indemnify the insured for the financial losses the latter may suffer due to the destruction of property or goods caused by fire during a specified period.

2.1.2 Marine Insurance

Marine Insurance is the oldest form of Insurance. Marine Insurance is a policy of repaying against the misfortunes of record dangers of the ocean. Marine Insurance plays a vital role in any shipping business by safeguarding you against the risk of damage or loss to cargo.

2.1.3 Vehicle Insurance

Vehicle insurance (also known as Motor/car/auto insurance) is Insurance purchased for cars, trucks, and other road vehicles. Its Primary objective is to protect against physical damage from traffic collisions and against liability that could also arise.

Globally, vehicle insurance is the biggest and the fastest growing general insurance portfolio, and India is no exception to it:

1) It accounts for over 45% of India's total general insurance premium income.

2) In the year ending 2006, the total non-life premium of the industry was about 28,000 crores out of which motor share was about 13,000 crores

3) However, the vehicle insurance business was only 25 crores at the time of nationalisation.

2.1.4 Credit Insurance

Credit protection safeguards providers against the gamble of non-installment of labour and products by their purchasers:

2.1.4.1 Domestic Risk: Buyer situated in the same country as the supplier.

2.1.4.2 Export Risk: Buyer situated in another country

Credit Insurance Shall Includes:

1) Non-Payment as a result of the insolvency of the buyer

2) Non-Payment after an agreed number of months after the due date (protracted default)

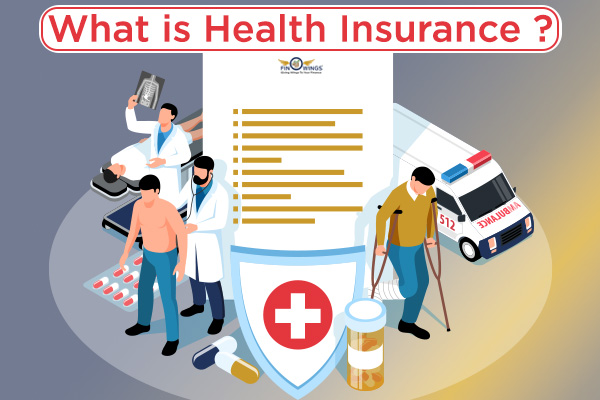

2.1.5 Health Insurance

Health care coverage is an insurance contract that covers the gamble of clinical costs in the circumstance of any awful emergencies. Health insurance prevents you and your family from suffering a financial loss due to an accident, illness, or disability. It can also provide income while you are disabled or in the hospital or cover medical or nursing care costs.

2.1.6 Fidelity Insurance

Fidelity insurance policy is the policy that covers the employer in respect of any direct financial losses which he may suffer as a result of employee dishonesty.

2.1.7 Burglary Insurance

Burglary means theft, robbery, or larceny. Robbery insurance is the policy that covers any misfortunes because of thievery. It is essential for a small business whose owners risk losing their livelihood due to theft. It is an add-on to other insurance policies.

2.2 Life Insurance:

2.2.1 Whole Life Insurance.

Whole life insurance means the Insurance in which the premium paid can be locked in for life. It can provide a cash value in addition to the death benefit. This policy never expires as long as you keep making premium payments. It is an expensive form of coverage.

2.2.2 Term Insurance

Term insurance is a type of Insurance that lasts for a specific period, known as a term before expiring. If you die before the term is up, your beneficiary, usually your family, receives death benefits as a tax-free lump sum of money that can be used for funeral costs, to pay bills, or for any other use. It is the type of Insurance that guarantees payment of a stated death benefit if the covered person dies during a specified term.

2.2.3 Money-back Plan

A cash-back plan is a unique life coverage strategy that falls under gift plans. Insurance language is called expected gift plans and is usually known as Cash Back Contracts. It gives protection cover and additionally occasional return at standard spans. In the event of the death of the insured during the policy term, the beneficiary will get full money.

2.2.4 Unit Linked Insurance Policy

A ULIP or unit-connected protection plan is a market-connected item that joins the best of protection and venture. It is an arrangement connected to the capital market and offers adaptability to put resources into value or obligation assets according to take a chance with craving.

3. Importance of Insurance:-

There are the following reasons why Insurance is Important:

3.1 To ease the pressure on a cherished one

3.2 To pay for your youngster's schooling

3.3 To safeguard your business

3.4 To take care of bills

3.5 To save the family home

3.6 To get your retirement

3.7 To leave a legacy

3.8 To cover the end-of-life costs

3.9 To give your family command over their monetary future

3.10 To give a wellspring of money during your lifetime

3.11 Pooling of hazard.

3.12 Federal retirement aide

3.13 Assurance against risk

4. The drawback of Insurance:-

4.1 Some of the time, insurance contracts don't give protection to old grown-ups or debilitated people

4.2 People picking protections before taking any protection should accept the assistance of a specialist while choosing protection organizations because of fakeness

4.3 The agreements of insurance contracts offer monetary help to individuals exclusively founded on different conditions

4.4 It might take an extended lawful technique to get the cases an individual has made.

4.5 No security from free dangers

5. History of Insurance:-

Insurance in India started in 1870, and the principal contract was given in 1870 by The European and The Albert. The main Indian protection was "Bombay Shared Affirmation Society Ltd shaped in 1870. As the Swadeshi development made up for a lost time, many more Indian organisations were framed. The insurance agency was nationalised in 1956. There were 170 insurance agencies and 75 fortunate asset protections, which got combined, and on 01st September 1956, Extra security Company of India was conceived, and LIC Act 1956 was passed. Further Broad Protection Business Act, 1972, and Protection Administrative and Improvement Authority Act.

The historical backdrop of protection is nearly about as old as the presence of people. A portion of the achievements connected with the history of protection are:

5.1 North of 5000 years back, Chinese merchants involved protection as a preventive measure against robbery. The freight of each boat used to be disseminated among different boats so that assuming one boat got lost or caught by privateers, the misfortune would be halfway.

5.2 The advancement of the life protections advertise as positive impact on financial development. The LIC was established in 1956 when the parliamentary of india passed the life protections of india act that natoinalized the private protections industry in india. LIC motto is in Sanskrit“Yoga kshemem waham yaham”which deciphered in english as your welfare is our duty.

5.3 The trade execution of life industry for the period finishing 31/12/1956 was 13 crores to begin with year premium on 9.5 lakh policies. The no of coordinate operators was 12387 within the year 1958

6. Present Structure of Insurance in India:-

The Opportunity for protection in India proceeds to be tremendous, providing the protection infiltration and thickness in india. FY22 saw a 4% YOY development in life protections, 11% YOY development in by and large common protections & 25% YOY development in wellbeing protections.

India is positioned 11th in worldwide protections commerce india’s share in worldwide protections showcase was 1.72% amid 2020 and add up to protections premium volume in india expanded by 0.1%. The showcase share of private segment companies within the non-life protections advertisements rose from 15% in FY 2004 to 49.3% in FY 2021.

Let's take a see at the best patterns that are forming the protections industry and how computerised advances are driving irreversible alter:

6.1 New Models, Personalised products

6.2 AI & Robotization for Quicker Claims

6.3 Advanced Analytics & proactiveness

6.4 Insurtech Partnership

6.5 Mainstreaming Blockchain

Protections Companies are for the most part organised in five wide divisions specially claims, fund, legitimate, showcasing and guaranteeing. Showcasing and endorsing are the “Yes” office, whereas claims and funds are “No” offices. The lawful division is frequently the official between these competing interests.

Toward the finish of the monetary year 2021, there were 67 back up plans working in india. Out of these 24 were life back up plans, 27 were general guarantors and five were independent wellbeing safety net providers.

7. Principles of Insurance:-

The Following principles of Insurance:-

7.1 Principle of utmost good faith

7.2 Principle of Insurable Interest

7.3 Principle of Indemnity

7.4 Principle of Contribution

7.5 Principle of Subrogation

8. Wrapping up:-

There are different protection items. Your necessities will change as per your life stage. Fabricate and reconfigure your protection portfolio. Audit your arrangements on a regular premise. Today a large portion of the insurance agency is enrolling specialists who are experts who can sell their unsought protection items. Organisations likewise give better arrangements in view of client needs and requests.