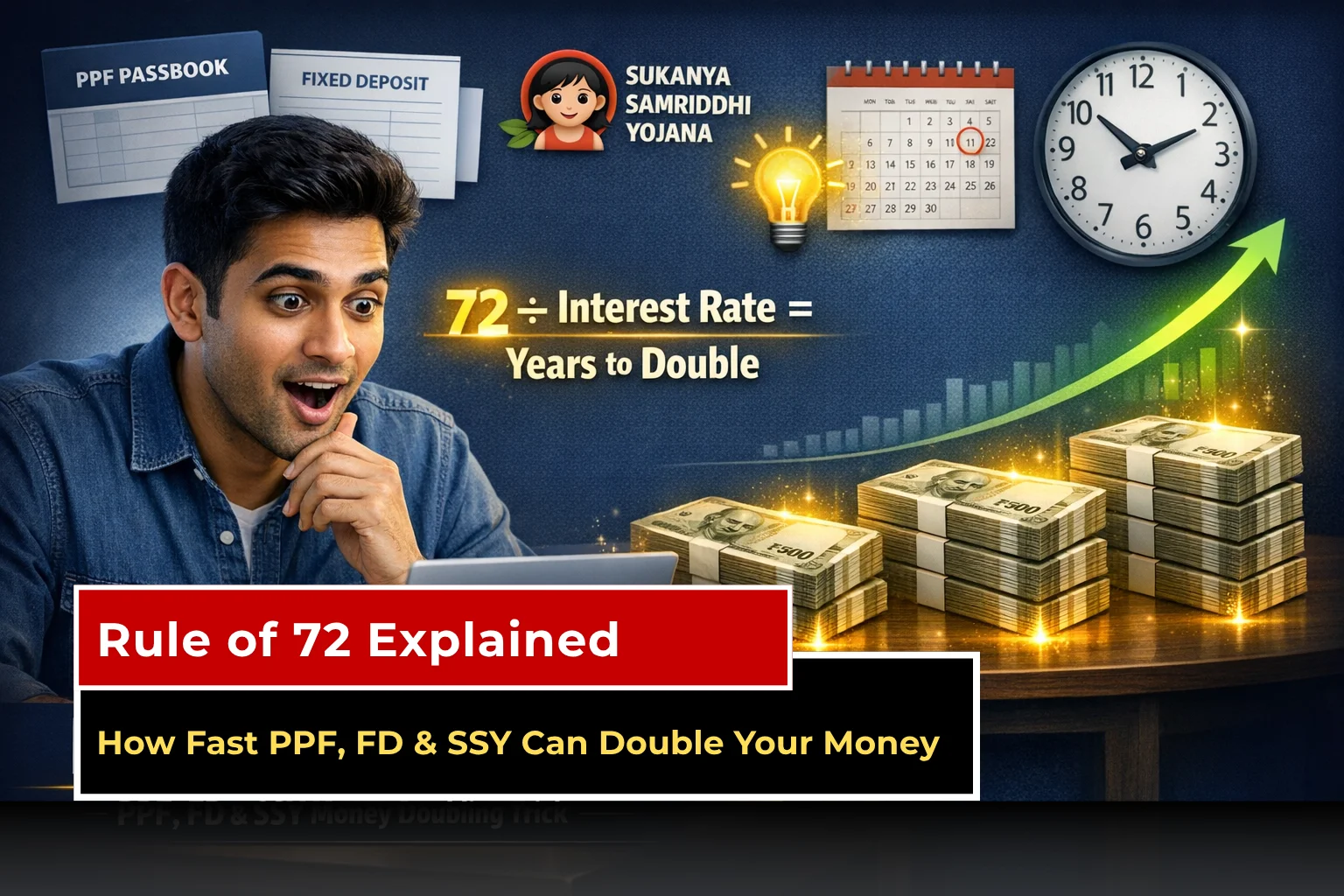

Imagine you are 30 years old and receive a ₹1 lakh bonus. You invest it wisely in a safe government scheme or bank deposit. Ten years later, without adding any more money, that ₹1 lakh has become nearly ₹2 lakh. Your money has quietly doubled itself.

This is not magic; it is the power of compound interest. And there is a simple trick called the rule of 72 that tells you exactly how many years it will take for your investment to double. In this easy-to-understand guide, we explain the rule of 72 and show how quickly your money can grow in three popular Indian options: PPF, FD, and SSY.

We will use simple words, real examples, a clear comparison table, and cover important points like limitations, inflation, taxes, and who should choose which scheme. By the end, you will feel confident using this investment-doubling rule for your own financial planning.

What Is the Rule of 72?

The rule of 72 is a quick mental maths shortcut. It answers one important question: “How many years will it take for my money to double at a given interest rate?”

Formula:

Years to double your money = 72 ÷ Interest Rate (%)

That’s all! No need for complicated calculators for rough estimates.

Example:

If your investment earns 8% per year, then 72 ÷ 8 = 9 years. Your money will roughly double in 9 years.

This works well because it comes from the compound interest formula. The full formula is:

Final Amount = Principal × (1 + Rate/100)^Time

But you don’t need to calculate that every time. The rule of 72 gives a fast, close-enough answer, especially for interest rates between 6% and 10%, which covers most safe Indian investments.

Why the Rule of 72 Is Useful for Beginners

Most Indians save in PPF for long-term goals, FD for medium-term needs, or SSY for their daughter’s future. These schemes use compound interest, so interest earns more interest over time.

The rule of 72 helps you see the speed of growth without any stress. It also lets you compare different options quickly. A small difference in rate (like 7% vs 8.2%) can mean a 1–2 year difference in doubling time.

Now let’s apply the rule of 72 to real schemes with current rates (as of April–June 2026 quarter).

PPF Returns: Safe and Tax-Free Growth

Public Provident Fund (PPF) is one of the safest options in India. The government backs it completely, and it offers compound interest calculated annually.

Current PPF returns: 7.1% per annum.

Using the rule of 72:

72 ÷ 7.1 ≈ 10.14 years

Actual doubling time (using full compound interest calculation): around 10.11 years. The rule is very close!

PPF has a 15-year lock-in (extendable), and the entire interest and maturity are tax-free (EEE status). It is ideal for retirement or long-term goals.

FD Interest Calculation: Flexible but Taxable

Fixed Deposits (FDs) are easy to understand. You put money into a fixed period and get guaranteed interest. Banks usually compound quarterly.

Current typical FD interest rates for general citizens: 6% to 7.5% (major banks). Some small finance banks offer up to 8%.

Let’s take a common 7% rate, for example.

Using the rule of 72:

72 ÷ 7 ≈ 10.29 years

Actual time: about 10.24 years.

For senior citizens, rates are higher (often 0.5% extra), so doubling happens a bit faster. However, FD interest is taxable as per your income slab, which reduces the effective growth.

SSY Growth: Fastest Option for Girl Child

Sukanya Samriddhi Yojana (SSY) is designed for girl children under 10 years. It offers high returns with full tax benefits.

Current SSY growth rate: 8.2% per annum, compounded annually.

Using the rule of 72: 72 ÷ 8.2 ≈ 8.78 years.

Actual time: nearly 8.8 years.

This makes SSY one of the fastest-doubling options among safe schemes. Like PPF, it also enjoys EEE tax status; investment, interest, and maturity are all tax-free. The account runs till the girl turns 21.

Still confused between safe schemes and market returns? Read our detailed guide on Sukanya Samriddhi vs Equity to make a smarter decision.

PPF vs FD vs SSY – Quick Comparison Table

Here is a simple data table to compare everything at a glance (rates as of April–June 2026):

|

Scheme |

Interest Rate |

Rule of 72 Doubling Time |

Actual Doubling Time |

Best For |

Tax on Interest |

Lock-in Period |

|

PPF |

7.1% |

10.14 years |

~10.11 years |

Retirement, long-term goals |

Fully tax-free |

15 years (extendable) |

|

FD (regular citizen) |

7.0% |

10.29 years |

~10.24 years |

Medium-term needs, flexibility |

Taxable |

As per the chosen tenure |

|

FD (Senior Citizen) |

7.5–8.0% |

9–9.6 years |

~9 years |

Seniors needing higher returns |

Taxable |

As per the chosen tenure |

|

SSY |

8.2% |

8.78 years |

~8.8 years |

Girl child’s education/marriage |

Fully tax-free |

Till the girl turns 21 |

Note: Actual times assume annual compounding. FD compounding is often quarterly, so real growth can be slightly faster. Rates can change every quarter.

Limitations of the Rule of 72 – Know the Truth

The rule of 72 is excellent for quick estimates, but it has some limitations:

- It works best for rates between 6% and 10%. For very low rates (like 2%) or very high rates (like 20%), the estimate becomes less accurate.

- It assumes fixed annual compounding and a constant rate. Real-life returns can change.

- It does not account for taxes, fees, or inflation.

- For monthly SIPs, the rule gives a rough idea but is not perfect because you add money regularly. Use a proper SIP calculator for exact projections.

- It works for guaranteed schemes like PPF/FD/SSY, but for market-linked investments (mutual funds, stocks), returns are not fixed, so actual doubling time can vary a lot.

If you’re planning regular investments instead of a lump sum, you can use a SIP Calculator to estimate how your monthly savings can grow over time.

Inflation-Adjusted Doubling: Nominal vs Real Return

Here is something important that many beginners miss. The rule of 72shows nominal doubling (before inflation). But inflation reduces purchasing power.

Suppose inflation is 6% per year. Then your real return = Nominal rate – Inflation.

For PPF at 7.1%: Real return ≈ 1.1%.

Using the rule of 72 on real return: 72 ÷ 1.1 ≈ 65 years to actually double your buying power!

This is why higher-rate options like SSY (real return ~2.2%) are powerful — they beat inflation better and double real wealth faster.

Always think about inflation-adjusted doubling when planning long-term goals.

Tax Impact on Actual Doubling Time

Taxes make a big difference:

- PPF and SSY: No tax on interest → full benefit of the rule of 72.

- FD: Interest is added to your income and taxed. If you are in 30% tax bracket, a 7% FD effectively gives only ~4.9% after tax.

- New doubling time: 72 ÷ 4.9 ≈ 14.7 years (much slower).

Senior citizens get some relief through higher FD rates and basic exemption, but still, tax-free options usually win for long-term doubling.

Who Should Choose PPF, FD, or SSY? (Decision Matrix)

- Choose PPF if: You want complete safety, tax-free growth, and can lock money for 15+ years. Best for retirement planning.

- Choose FD if: You need money in 1–5 years, want flexibility, or are a senior citizen looking for higher rates. Good for emergency funds or short goals.

- Choose SSY if: You have a girl child below 10 years. It offers the fastest SSY growth among safe options with full tax benefits. Ideal for education or marriage expenses.

- Mix them: Many smart investors use all three — SSY for daughter, PPF for retirement, and FD for medium goals.

For non-guaranteed returns (like equity mutual funds), the rule of 72still works as a rough guide if you assume average returns (example: 12% → doubles in 6 years), but expect ups and downs.

Real-Life Example: How the Rule of 72 Helped a Family

Rajesh (35 years old) had ₹3 lakh to invest. He used the rule of 72and split it:

- ₹1 lakh in PPF (7.1%) → doubles in ~10 years

- ₹1 lakh in FD (7%) → doubles in ~10.3 years

- ₹1 lakh in SSY for his daughter (8.2%) → doubles in ~8.8 years

After 10 years, his money grew to almost ₹6 lakh. He now checks rates every quarter and teaches his friends the same simple trick.

Smart Tips to Make Your Money Double Faster

- Start as early as possible — time is your biggest friend in compounding.

- Check the latest rates every quarter (the government updates small savings schemes).

- Consider your tax slab before choosing taxable options like an FD.

- For monthly SIPs, the rule of 72gives direction, but use online calculators for precise future value.

- Always compare nominal return with inflation to understand real growth.

- Diversify: Don’t put everything in one scheme.

Conclusion

The rule of 72is a simple yet powerful investment doubling rule that every beginner should know. It turns confusing numbers into clear answers and helps you compare PPF returns, FD interest calculation, and SSY growth easily.

Whether you prefer the safety of PPF, the flexibility of FD, or the fast SSY growth for your daughter, this rule gives you confidence to decide. Remember its limitations, factor in taxes and inflation, and start investing today.

Your future self will thank you when your money doubles not once, but again and again through the magic of compound interest.

(Sources: ET, NSI India, Clear Tax and Others)

DISCLAIMER: This blog is NOT any buy or sell recommendation. No investment or trading advice is given. The content is purely for educational and information purposes only. Always consult your eligible financial advisor for investment-related decisions.

.jpg)