Every parent wants to secure a child's future, be it for education, skill development, marriage, or overall finances. However, with increasing educational costs, inflation, and competition, planning accordingly has become highly essential. This is where a parent choosing the right child investment plans becomes a smart and strategic move.

In this blog, we will discuss the child investment plans along with the best SIPs, mutual funds, and long-term strategies. This will give a parent and child a real chance at building a financially secure future.

The Importance of Child Investment Planning

The costs surrounding a child's future are astonishing:-

-

Coaching classes.

-

School and college fees.

-

Skill development courses.

-

Higher education overseas.

-

Start-up aspirations or career goals.

The earlier a parent starts planning for the child's future, the less worrying the educational investment becomes. This is all due to the power of compounding.

1. SIPs for A Child's Future – Easiest Way to Create Wealth Over Time

Systematic Investment Plans (SIPs) are a common choice for most parents. As they help in:

-

The monthly investment is low.

-

Compounding is significant in the long run.

-

The investment amount can be increased to a desired level.

-

Growth can be linked to the market.

Determining the best SIP for a child's future largely depends on the number of years remaining. The longer the time, the better the compounding that happens over time.

Best Child SIP Plans

Below are the SIPs best for long-term child objectives.

Equity Mutual Fund SIP - Has high growth potential, and is thus ideal for longer time horizons (10+ years). Great for funding higher education.

Index Fund SIP - Has a low cost, is quite consistent, and tracks Nifty/Sensex. Very good for systematically creating wealth over the long term.

Hybrid SIP (Equity + Debt) - Has a balanced risk profile; good for medium-term objectives (5–10 years). Great for funding gadgets, early education fees, and so on.

Debt SIP (Short-term goals) - Has stable returns; great to plan for expenses in the coming 2 to 4 years. These child SIP plans allow risk to be spread and returns to be maximised based on your time horizon.

2. Child Mutual Fund Plans – Tailored For Kids' Needs

For years now, numerous AMCs have been providing fully dedicated Child Mutual Fund Plans, also known as Child Gift Funds/Child Advantage Funds. These plans offer the following:

-

Lock-in period (to ensure withdrawal cannot occur prematurely).

-

Long-term wealth strategy.

-

Hybrid (equity + debt).

-

Designed as an investment with specific goal(s).

Child Mutual Fund Plans

For parents looking for:

-

Long-term investment with added discipline.

-

Automatic stability from hybrid allocation.

-

Lock-in period to reduce the chances of withdrawal.

Ideal for child education investment targeted for expenses needed within a 5–15 year time frame. These funds work well for child education investment, expected expenses after 5+ years.

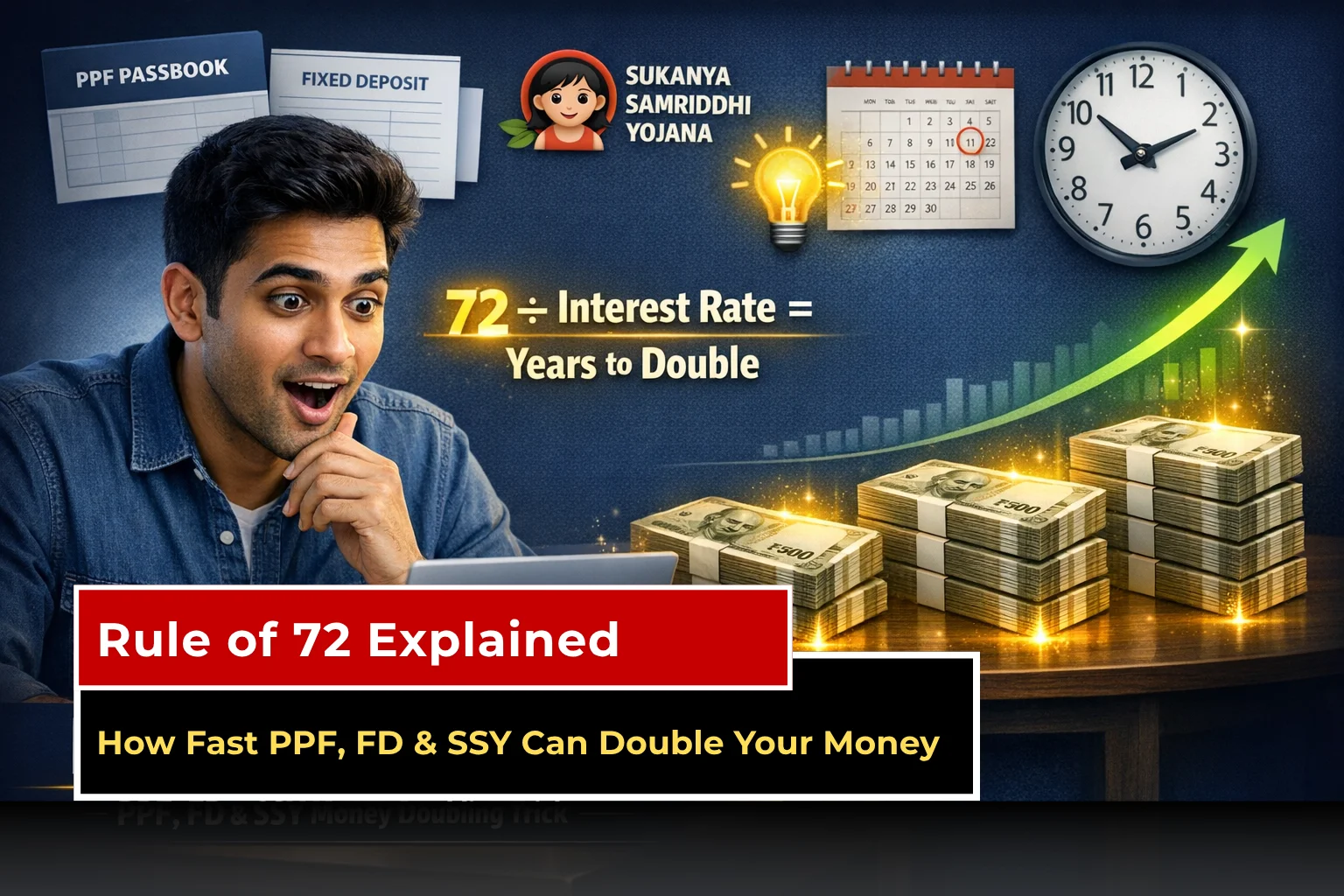

3. Sukanya Samriddhi Yojana (SSY) – Investments for a Girl Child

SSY is among the most well-known for the child's future investment plans. Most people in the investment community love recommending this scheme, especially for female offspring.

Key Benefits

-

Backed by the government.

-

8%+ interest rate (subject to change 4 times a year).

-

Maturity is not taxed.

-

Section 80C also supports the deduction from tax.

SSY must be in your portfolio if your child is a girl.

4. Public Provident Fund (PPF) – A Safe Long-Term Plan

For long-term goals relating to children, this scheme truly shines as a low-risk investment option. PPF is a government-backed scheme, which makes this a safe choice.

Why PPF is Good for Kids:

- 15-year lock-in

- Tax-free withdrawal

- High compounding

- Safe & stable

PPF is a good foundational layer for child investment plans for parents who prefer stability over returns.

5. National Pension System (NPS) – For Long-Term Child Goals

If you want to create a retirement-like corpus for your child’s future, NPS can also be considered.

Benefits:

- High equity exposure

- Low charges

- Long-term compounding

- Tax benefits

Though primarily a retirement product, disciplined parents also use it as part of their child future investment plans.

6. Direct Equity – High Risk, High Reward

While not suitable for everyone, some parents invest a small portion in stocks to build a long-term portfolio for their child.

Examples:

- Bluechip stocks (stable)

- High-growth midcaps (aggressive)

This should be only a small portion of the child's investment basket due to the high risk involved.

How to Choose the Best Child Investment Plans

When selecting the right investment option, consider your child’s age, your risk tolerance, Future goals, and Further studies abroad. Startup? wedding?, expected inflation, for further studies, the inflation is approximately 8-12% each year, Monthly savings capacity

Based on your earnings and financial plan, set your SIP amount.

Illustration Investment Plan for Child Future (Age 1-18 years)

|

Child Age |

Ideal Investment |

Reason |

|

0–5 years |

Equity SIP + Index Funds |

Maximum compounding |

|

5–10 years |

Hybrid Funds + SSY/PPF |

Balanced growth |

|

10–15 years |

Largecap + Hybrid SIP |

Lower volatility |

|

15–18 years |

Debt funds + PPF maturity |

Safe for final withdrawal |

The framework effectively provides growth and stability in the long run.

Why SIP is the Optimum Plan for Child Future

Out of all plans, the best SIP for child future will provide you with predictability in investing, returns higher than inflation, moderate risk for longer durations, benefits of compounding. SIPs form the foundation of children's future investment plans for the majority of parents.

Conclusion

A parent’s greatest gift to a child is planning for their future. Be it child SIP plans, child mutual fund plans, government schemes like SSY and PPF, or a diversified investment portfolio, the first step is starting early and staying consistent.

With education and lifestyle costs on the rise, the child investment plans available today provide several opportunities to build a child’s financial foundation and support their education and future career goals. By aiming for the right mix of SIPs, mutual funds, and secure long-term schemes, you can successfully be on the path to fulfilling your child’s dreams.

DISCLAIMER: This blog is NOT any buy or sell recommendation. No investment or trading advice is given. The content is purely for educational and information purposes only. Always consult your eligible financial advisor for investment-related decisions.