Introduction :

On February 13, Nirmala Sitharaman presented the New Income Tax Bill in Lok Sabha. This Bill is set to replace more difficult phrases such as ‘assessment’ and ‘the previous year’ with ‘tax year’, as part of restatement and removal of explanatory clauses that sought to simplify the provisions. With new tax rules, the New Income Tax Bill 2025 does not come without limitations.

With 23 chapters, 536 sections, and 16 schedules, the entire bill is composed of 622 pages. This differs from the existing Income Tax Act of 1961, with only 298 sections and 14 schedules, and strives to simplify the language of the Act rather than impose any new taxes.

New Income Tax Bill 2025

1) Revised Income Tax Slabs:

The entire class of taxpayers with an annual salary of Rs.12 lakh will be exempt from taxation. These changes, alongside the updated tax slabs and higher exemptions, are likely to stimulate expenses and savings amongst the middle class while also increasing the amount of money available for them.

New tax Slabs

2) Time Limit For Filing Updated Income Tax Returns:

The duration for filing updated returns has been increased from two years to four years. This change will permit taxpayers more time to correct any mistakes made on their Returns. The government is certain that tax compliance will be made simpler through these measures without causing inequality among taxpayers.

3) Capital Gains Tax And Tax Brackets Remain Unchanged:

There will be no modifications to short-term capital gains (STCG tax) and long-term capital gains (LTCG tax) taxation under the provisions of the new Income Tax Bill. Short-term capital gains concerning equities, funds, and business trusts like REITs and InvITs will remain at 20%. There is no change to the current income tax slabs which means all taxpayers will remain under the same rates they were before.

4) More Restrictive Provisions For Digital Virtual Assets:

The bill incorporates provisions for VDAs where cryptocurrencies and non-fungible tokens are categorized as undisclosed income like money and bullion for searches. The objective here is to tighten control over the marketing of the digital assets.

5) Tax Law provisions have been consolidated.

The focus of the new Bill will be to cut the sections down by 25 to 30 % which will in turn simplify the tax code. This is expected to minimize the burdens of compliance as well as disputes.

6) Residency Status

While keeping the existing taxation practices, the newly proposed bill addresses issues on total income scope. As per the earlier provisions, Sections 5 and 9 of the Income Tax Act, 1961, provided that Indian residents were chargeable to tax on their global income, whereas non-residents were chargeable to tax only with the income sourced in India.

7) New Terminology 'Tax Year' For Financial Year And Assessment Year Related Systems:

With this Bill, the term tax year will be introduced with its definition along with the removal of caps and definitions that were previously utilized. This resolves the unnecessary complexity and volume of language.

While keeping the existing taxation practices, the newly proposed bill addresses issues on total income scope. As per the earlier provisions, Sections 5 and 9 of the Income Tax Act, 1961, provided that Indian residents were chargeable to tax on their global income, whereas non-residents were chargeable to tax only with the income sourced in India.

8) Strict Virtual Digital Assets Rules

This income tax bill, known to virtually capture every industry segment, under Clauses 67 to 91 relates to special provisions for the taxation of “virtual digital assets” and contains an update of the low rate of tax on such income.

The so-called tax ‘loophole’ was defined so that digital assets, particularly cryptocurrency, are adequately addressed under the law. It defines “virtual digital asset” and “electronic mode” to embody the emerging phenomenon of digital assets and cryptocurrency in the context of modern money.

9) "Increased Accountability for Non-Profit Tax Exemptions"

Non-profit organizational purposes were legalized, under sections 11 to 13, to allow for income tax exemption for specified charitable activities but there was no compliance post such exemptions.

The new bill, in Clauses 332 to 355, split limits that imposed a public trust obligation towards better-defined bounds for deemed income, compliance entire balance of activities for the one defined as business and revenue or the general activities of corporations. This expands further the new bill’s mandate toward increasing compliance without detailing much.

10) Startups, Digital Businesses, and Revisions to Capital Gains

The new tax bill captures the deductions made before as well as other new provisions designed for the support of startups, digital enterprises, and investment in renewable energy under Clauses 11 to 154.

Alterations have also been made to the definitions of capital gains tax. Taxing as per the old law, Sections 45 to 55A of the Act sliced capital gains into short-term and long-term capital gains, by the holding periods of the assets with a special tax rate for the securities.

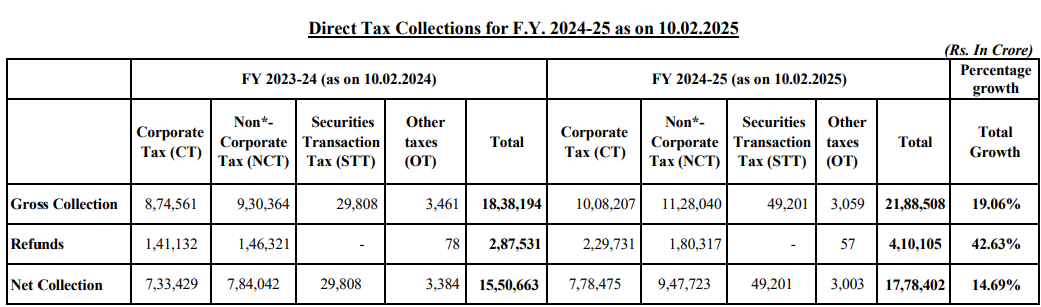

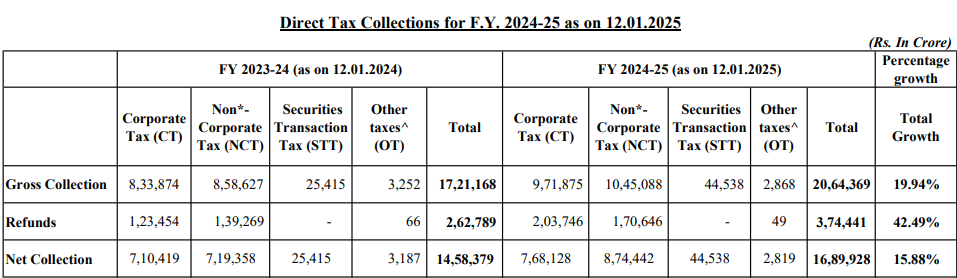

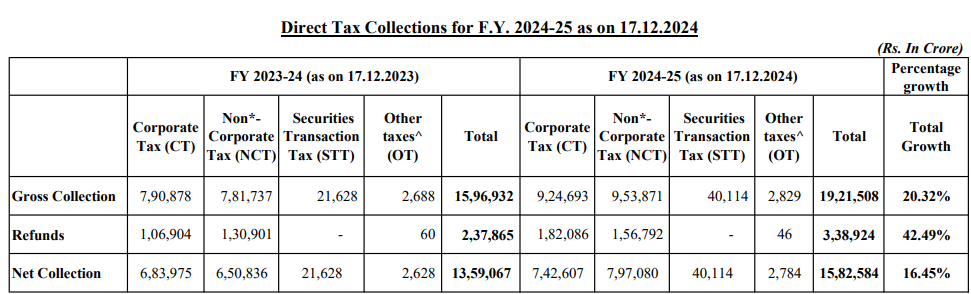

Direct Tax Collections for three Months of F.Y. 2024-25

(Source: TINMIS)

Conclusion:

The New Income Tax Bill 2025 is an effort to simplify the tax laws by using clearer terminology and reducing convoluted sections. It provides for the introduction of new tax slabs and an extended time frame for the filing of updated returns, whereas it does not change capital gains tax. It further tightens digital assets cryptocurrency regulations and ensures better compliance for non-profit organizations. Moreover, it gives support to startups, e-businesses, and investments in renewable energy. It does not impose any new tax burdens but strives to enhance clarity and fairness in the area of taxation. The Bill is designed to simplify tax filing and enhance compliance among taxpayers.