Value at Risk (VaR) is used to forecast the biggest potential losses over a certain time period and has been dubbed the "new science of risk management."

VaR is a tool frequently used in investment research by commercial banks and financial institutions to gauge the size and likelihood of future losses in portfolios. In addition, VaR is a tool used by risk managers to gauge and manage the degree of risk exposure.

What is Value at Risk?

Value at Risk (VaR) is a statistic that measures how much money could be lost by a company, portfolio, or position over a certain period of time. Investment and commercial banks most frequently use this indicator to assess the size and likelihood of prospective losses in their institutional portfolios.

VaR is a tool used by risk managers to gauge and manage the degree of risk exposure. VaR calculations can be used to assess individual holdings, entire portfolios, or the overall risk exposure of an organization.

Elements of Value at Risk (VaR)

An investor's primary concern is the likelihood of losing money, and volatility is the classic risk indicator. The VaR statistic can handle the following issues because it includes three parts: a period, a confidence level, and a loss amount, or loss percentage:

With a 95% or 99% level of confidence, how much money can I anticipate losing in the upcoming month?

What is the highest percentage loss I may reasonably anticipate during the coming year, with a 95% or 99% certainty?

High levels of confidence, a time frame, and an estimate of investment loss are the primary issues that are included in the questions.

Value at Risk (VaR) characteristics include:

-

VaR is probability-based and enables users to understand potential losses at different levels of confidence.

-

Because it employs the potential rupee loss indicator, it provides a consistent way for analysts to compare financial Risk across various portfolios, assets, and even business lines.

-

VaR is calculated using a standard time horizon, making it possible to quantify potential losses over a certain time frame.

-

The industry standards or reporting norms recommended by the regulators are typically the basis for the confidence level selection. The sort of asset being examined will determine the time horizon to be used, for instance:

-

It can be estimated for any horizon on a common stock depending on the trade frequency or user requirements.

-

VaR can only be calculated for turnover or until the portfolio holdings remain constant. As soon as a holding changes or, to put it another way, if a trade is recorded in the portfolio, the VaR must be recalculated. As a result, a portfolio's time horizon depends on how frequently its assets are traded.

-

The available time ranges for a business study may rely on employee assessment cycles, significant decision-making moments, etc.

-

Tax and regulatory requirements

-

Evaluations of external quality, etc.

The two factors, i.e., time horizon and confidence level, must be constant for all the portfolios being compared in order to compare VaR between two portfolios, business lines, or assets.

Methods of Calculating Value at Risk:

-

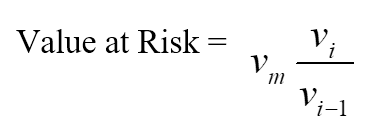

Historical Approach

The simplest way to determine Value at Risk is to use past data. First, each day's percentage change for each risk factor is computed using market data from the previous 250 days. Then, for each % change, 250 future value scenarios based on the most recent market prices are offered.

The portfolio is valued using complete, non-linear pricing models for each of the possibilities. It is assumed that the third worst day will have a VaR of 99%.

Where:

-

vi is the number of variables on ith day

-

m is the number of days from which historical data is taken

-

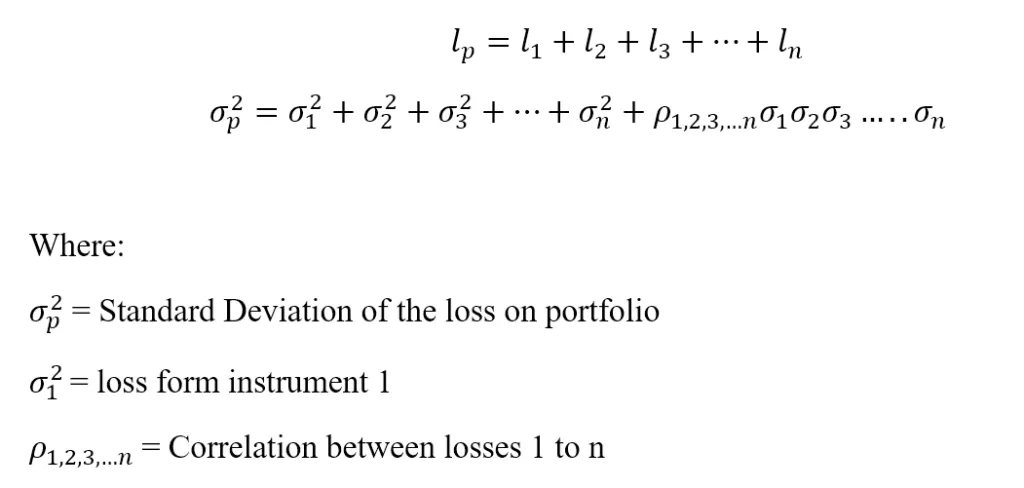

Parametric Method

The variance-covariance method is another name for the parametric method. It counts on the results having a normal distribution. Therefore, an expected return and a standard deviation must both be estimated.

The parametric approach works best for risk-measuring issues where the distributions can be accurately predicted and known. However, the approach is unreliable when the sample size is very tiny.

Let the loss for a portfolio with 'n' instruments in it be 'l.'

Monte Carlo Methods

The Value at Risk (VaR) is determined using the Monte Carlo method by establishing a variety of hypothetical future rate scenarios, estimating the change in value for each scenario using non-linear pricing models, and then computing the VaR based on the worst losses.

Numerous risk measurement issues can be solved using the Monte Carlo method, particularly when dealing with complex elements. However, it is predicated on risk factors having a defined probability distribution.

Marginal Value at Risk (MVaR)

The amount of extra Risk that a new investment in the portfolio adds is calculated using the marginal value at risk (MVaR) approach. Fund managers can better comprehend portfolio changes brought on by the removal or inclusion of a certain investment by using MVaR.

Even while an investment may have a high Value at Risk on its own, if it has a low correlation to the rest of the portfolio, it may add considerably less Risk than it would on its own.

Incremental Value at Risk

The amount of uncertainty added to or withdrawn from a portfolio due to buying or selling an investment is known as incremental VaR. The standard deviation and rate of return of the portfolio, as well as the rate of return and portfolio proportion of each investment, are taken into account while calculating incremental VaR. (The portfolio share is the proportion of the overall portfolio that each investment makes up.)

Value Conditional on Risk (CVaR)

The predicted shortfall, average value at Risk, tail VaR, mean excess loss, or mean shortfall are other names for this. VaR is expanded upon by CVaR. In a distribution, calculating CVaR can be used to estimate the average loss that occurs above the value at the risk point. The better, the smaller the CVaR.

Benefits from Value at Risk (VaR)

-

Simple to comprehend

A single metric called "Value at Risk" describes the degree of Risk present in a certain portfolio. Value at Risk is expressed as a percentage or as price units. This makes the interpretation and comprehension of VaR rather straightforward.

-

Relativity

All asset classes, including bonds, shares, derivatives, currencies, etc., are subject to Value at Risk. As a result, VaR is a simple tool that various banks and financial organizations can use to evaluate the profitability and Risk of various investments and allocate Risk in accordance with VaR.

-

Universal

The Value at Risk statistic is frequently employed, making it a recognized benchmark when purchasing, disposing of, or recommending assets.

Limitations of Value at Risk

-

Huge portfolios

One must ascertain the Risk and return of each asset and their correlations to calculate the VaR for a portfolio. VaR calculation becomes increasingly challenging as a portfolio's size or asset diversity increases.

-

Different approaches

Different methods for computing VaR can produce different outcomes for the same portfolio.

-

Considerations

One must make some assumptions and utilize them as inputs while calculating VaR. The VaR figure is invalid if the assumptions are incorrect.

Examples of Value at Risk:

-

A ground-breaking report on derivatives practices was released by The Group of 30 in 1993. It had an impact and shaped the newly-emerging discipline of financial risk management. It appears to be the first publication to introduce the term "value-at-risk" and promote its use by derivatives traders.

-

The first thorough explanation of value-at-risk was published in detail by JP Morgan in 1994 as part of their free Risk Metrics service. This was done to encourage institutional clients of the company to employ value-at-risk. The service included an online daily updated covariance matrix for several hundred significant elements as well as a technical manual outlining how to create a VaR measure.

-

Market risk capital requirements for banks were adopted in 1995 by the Basel Committee on Banking Supervision. These were based on a rudimentary value-at-risk calculation, but the committee also permitted the use of banks' own proprietary VaR calculations under certain conditions.

Conclusion:

Every decision-making process should include calculating the worst-case scenario or value at Risk (VaR). It enables the management or investors to assume the greatest exposure, act remedially, or select from a range of possibilities. However, the computation period utilized by various VaR methods can produce varying findings that must be examined with regard to total risk-return potential.

72.jpg)