.jpeg)

Introduction

Today, let's take a closer look at a company operating in the gold industry - Rajesh Exports. This company holds a prominent position in the world, but is its reality in line with our expectations? Let's delve deep to understand.

Unveiling the Mystery

Why is Rajesh Exports, the behemoth claiming to refine 35% of the world's gold, experiencing a downhill slide? The past six months have witnessed a staggering 50% dip in its shares, and the current standing at 350 only adds to the intrigue.

The Global Gold Maestro

Rajesh Exports, not just a name but a force in the gold industry, is known for refining a significant chunk of the world's gold. But hold on – if you're holding shares bought at a premium, should you stick around, average out, or make a swift exit? And what about the newcomers eyeing this golden opportunity?

Buckle up as we explore these questions and more, promising you answers that might just redefine your investment strategy.

Detailed Video

Behind the Scenes: The Business Model

Before we don our detective hats, let's understand the intricate dance of Rajesh Exports' business model. From importing raw gold from the world's mining giants to its minimal foray into mining (a mere 1 ton per year), this company processes a whopping 900 tonnes of gold annually. It doesn't stop there – the refined gold transforms into bullions, finding its way to central banks and companies dealing in these glittering assets.

But wait, there's more – the company also crafts exquisite gold jewelry, adorning both wholesale and retail markets. Shubh Jewellers, the brand under which they retail, boasts over 70 showrooms across India. And if that wasn't enough, Rajesh Exports exports its golden creations to the UAE and Europe.

A grand setup, a global presence – on the surface, everything seems splendid. But as we peel back the layers, the tale takes an unexpected turn.

The Fundamentals Unveiled

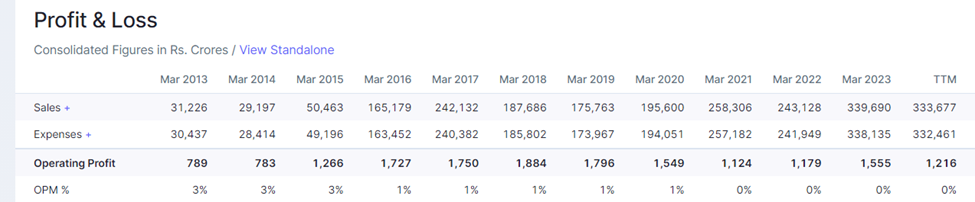

Sales and profit, the heartbeat of any business, should tell us the true story. Yet, Rajesh Exports' cash flow has been performing an unsettling dance in the negative zone for three consecutive years. A seemingly thriving business is struggling to generate positive cash flow – the first red flag.

Diving deeper, we discover that while the company sales figures (around 2.5 lakh crores in the last three years), the operating profit is 1100 crores.

To put it bluntly, a company of such scale should be yielding more significant profits. The operating profit margin, a meager 0.5%, raises eyebrows and sends the second red flag fluttering.

Cracking the Code: Cost Analysis

As we venture further into the labyrinth, the costs come into focus. Rajesh Exports' material cost stands at a whopping 99%.

Can a company claiming to refine 35% of the world's gold afford such a lopsided cost structure? Peer companies like Kalyan Jewellers and Senco Gold, with lower sales volumes, maintain a more balanced employee cost ranging from 2% to 4%.

The employee cost conundrum becomes even more intriguing when we discover that the company operated with a mere 181 employees in 2021, a number that dwindled to 135 in 2022. Can a giant corporation thrive with such minimal staffing?

Inventories: A Goldmine or a Quandary?

In the inventory chamber, Rajesh Exports displays 4500 crores in work in progress and approximately 2000 crores in finished goods. A question arises – how can a company with such low manufacturing costs (less than 1% compared to sales) efficiently process such vast amounts of raw materials?

Auditor's Negligence: Unmasking the Foreign Subsidiary Conundrum

The plot thickens as we delve into the company's structure. Rajesh Exports' 100% foreign subsidiary, REL Singapore PTE, raises eyebrows. While the consolidated sales figure boasts 3 lakh crores, deducting the sales of foreign subsidiaries leaves us with a mere 6000 crores attributed to Rajesh Exports alone.

The auditors, it seems, have left some stones unturned. They admit to auditing only the Indian arm of Rajesh Exports, neglecting the financials of its foreign subsidiaries. A substantial amount of 2.4 lakh crores hangs in the balance, with authenticity under scrutiny.

Mismatch of Figures: Balancing the Books or Walking a Tightrope?

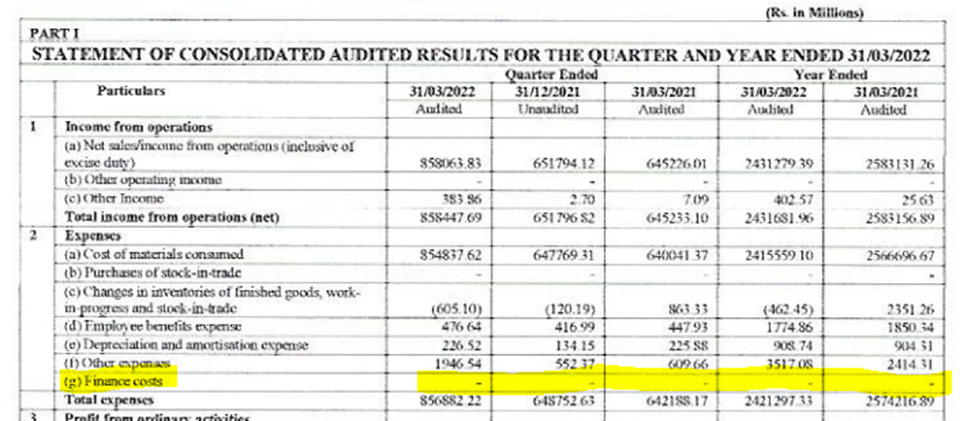

In the world of finance, numbers are sacred, or so we believe. However, Rajesh Exports seems to be dancing to its own tune. The financial statements published do not align with the figures in the annual report. Finance costs, for instance, are a ghost in the financial statements but come alive in the annual report – 142 crores in 2021 and 90 crores in 2022. A significant discrepancy raises the third red flag.

Non-Compliance of SEBI's Regulations: Navigating Uncharted Waters:

SEBI's regulations form the rulebook for listed companies, ensuring transparency and accountability. Rajesh Exports, however, seems to be playing by its own rules. The company fails to follow the prescribed format for quarterly results, omitting a half-year cash flow statement and audit report.

In a bid to maintain mystery, the company refrains from providing a comparative cash flow statement and audit report when announcing results. A clarion call from NSE forces them to resubmit the cash flow statement – a move that raises questions about corporate governance.

Conclusion

As we stand at the crossroads of analysis, one thing is clear – Rajesh Exports is not the golden goose it appears to be. The market, sensing the ripples beneath the surface, has initiated a value adjustment, resulting in the continuous fall of its share price.

So, dear readers, what are your thoughts on this riveting tale of Rajesh Exports? Do you agree with the analysis, or do you see a different plot twist on the horizon? Share your insights in the comments section.

As we bid adieu to this thrilling financial odyssey, stay tuned for more adventures in the world of fundamental analysis.

Disclaimer

Please note that this blog is not a recommendation for buying or selling any stock. We encourage readers to conduct thorough research, consider their risk tolerance, and consult with financial advisors before making investment decisions.

Ankit | Posted on 14/01/2024

I have shares at 558, do you think the price will recover? Stock is hovering at 370 only.